Home

About FRP Institute

About ICERP

About ICERP Show

Organising Committee

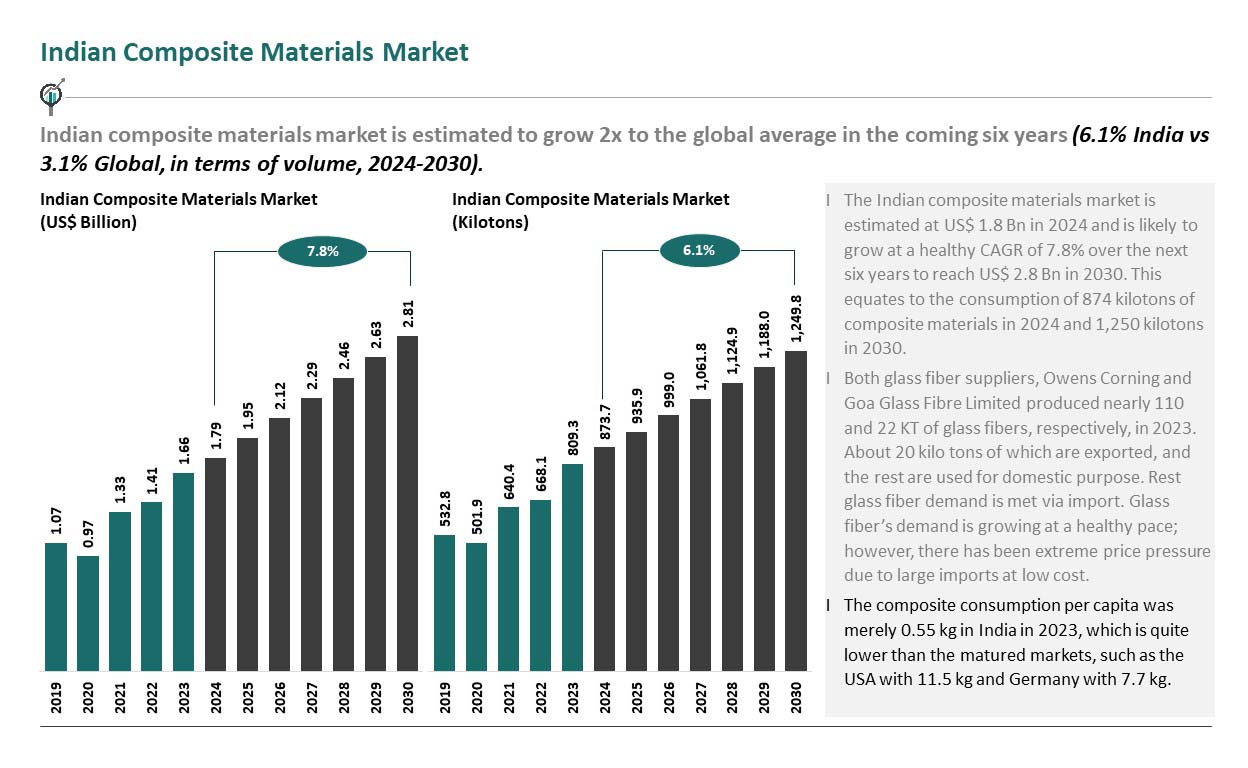

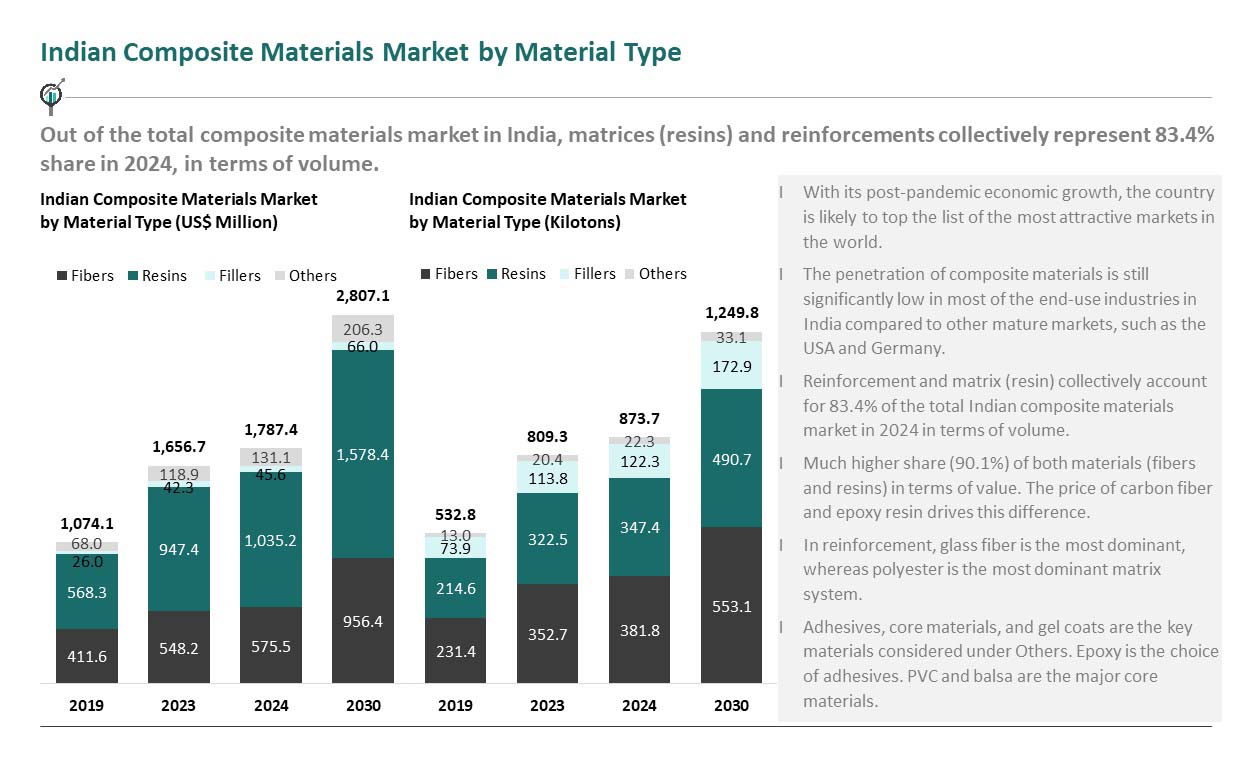

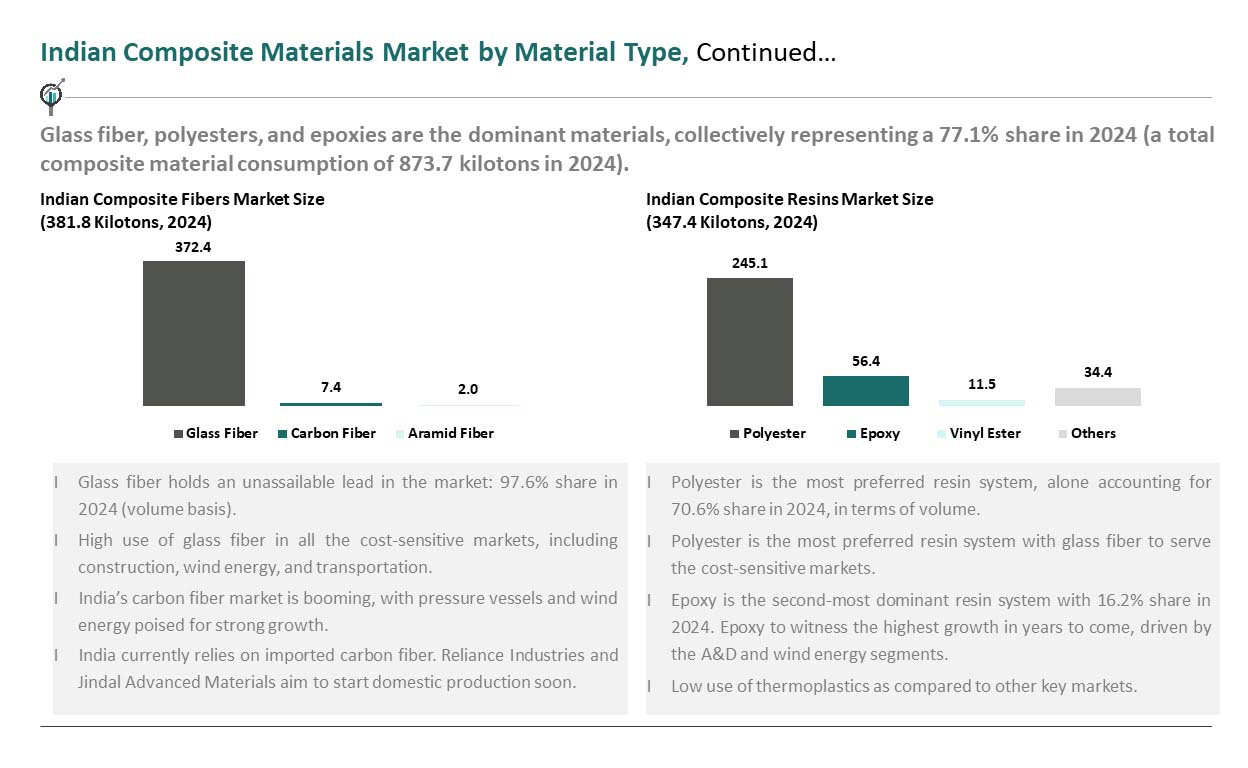

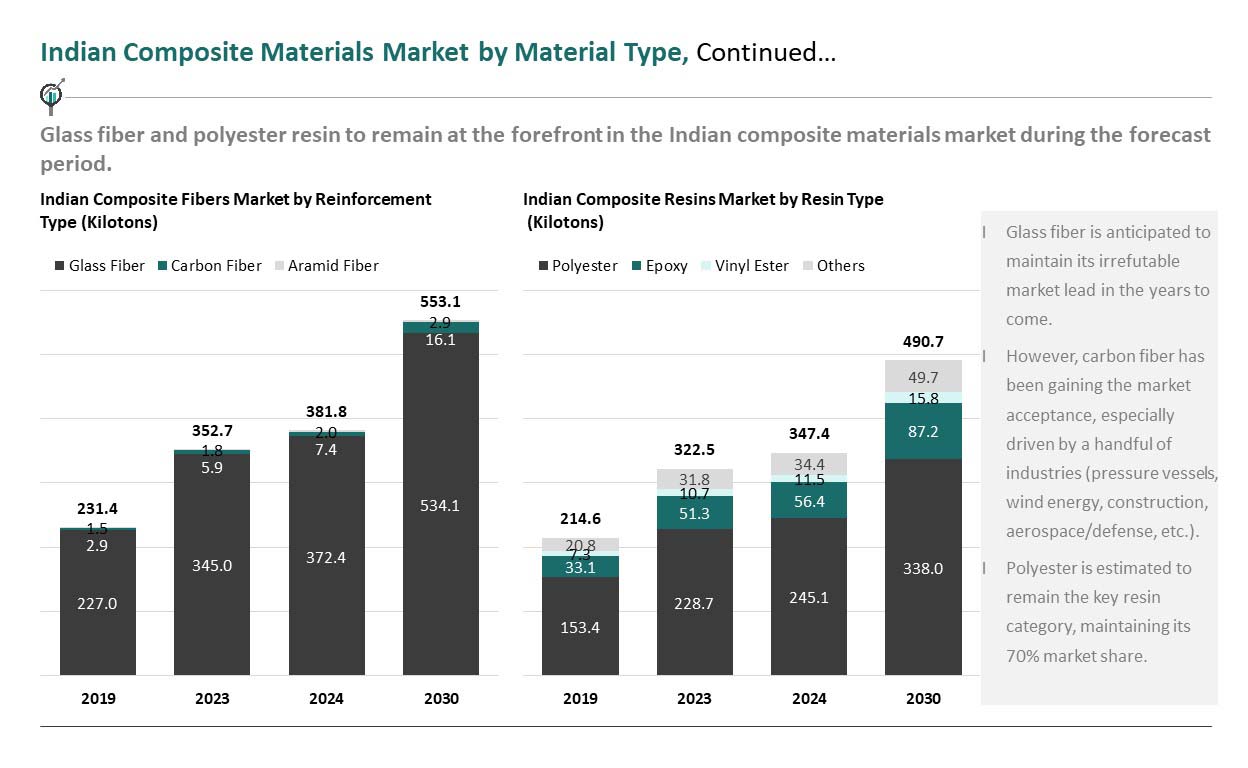

Indian Composites Industry Outlook

For Exhibitor

Interactive Floor Plan

Schedule Meeting

Floor Plan

Exhibitor List

Technical Sale Presentation Schedule

Exhibitor Manual

Create your own Signature

Booth Charges

Showcase your Product

Exhibitor Registration Form

Exhibitor Profile

Sponsorship Opportunities

Overall Venue Map

Mumbai & Around

For Visitors

Schedule Meeting

Interactive Floor plan

Exhibitor List

Visitor Registration Form

Overall Venue Map

Mumbai & Around

Conference Program

About Conference

Conference Schedule

Call for papers

Delegate Registration Form

Overall Venue Map

ICERP-JEC Innovation Awards

Media

Photo Gallery

Video

Contact Us

Indian Composites Industry Outlook

HOME

>

About ICERP

>

Indian Composites Industry Outlook

Follow:

Exhibition Grounds

Create your own Signature

Getting there

Media

Photo Gallery

Video

News

Retrospective

Media Centre

Contact Us

PGresponse

About FRP Institute

Coming Soon

ICERP-JEC Innovation Awards

About Conference

About ICERP

About ICERP Show

Indian Composites Industry Outlook

Organising Committee

Organisers

Showcase your Product

Process Demo

Exhibitor Profile

Privacy Policy

Conference Schedule

Delegate Registration Form

Exhibition Floor Plan

Conference Program Schedule

Indian Delegate Form

Foreign Delegate Form

Overall Venue Map

Arrival & Stay

Accommodation & Tour

Mumbai & Around

Exhibition Grounds

Call for papers

ICERP 2025 EXHIBITOR LIST

HOME

SCHEDULE

HOTEL SUGGESTIONS NEAR TO VENUE AND INTERNATIONAL AIRPORT

Industry Trends

Exhibitor List

The ICERP

Press releases

FAQ’s

For Exhibitor

Floor Plan

Booth Charges

Indian Exhibitor Form

Exhibitor Registration Form

Foreign Exhibitor Form

Overall Venue Map

Sponsorship Opportunities

Arrival & Stay

Accommodation & Tour-copy

Mumbai & Around

Venue

accordion

Getting there

Venue

testingform

For Visitors

Visitors Registration Form

Exhibitor Floor Plan

Overall Venue Map

Arrival & Stay

Accommodation & Tour-copy2

Mumbai & Around

Upcoming Show

Exhibitors Profile

Exhibition Grounds

Sponsorship Forms

Newsletters

Newsletters

DOWNLOAD

TECHNICAL SALES PRESENTATIONS SCHEDULE

DOWNLOAD

BROCHURE

DOWNLOAD

FLOORPLAN

BOOTH

RATES

INTERACTIVE

FLOOR PLAN

For Exhibitor

SCHEDULE

MEETING

DOWNLOAD

INDIAN EXHIBITOR

REGISTRATION FORM

DOWNLOAD

FOREGIN EXHIBITOR

REGISTRATION FORM

ONLINE

EXHIBITOR

REGISTRATION FORM

CREATE

YOUR OWN

SIGNATURE

For Visitor

ONLINE

VISITOR

REGISTRATION FORM

EXHIBITOR

LIST

SCHEDULE

MEETING

For Conference Delegate

ONLINE

DELEGATE

REGISTRATION FORM

CONFERENCE

PROGRAM

SCHEDULE

QUICK ACCESS

FREE ONLINE

VISITOR REGISTRATION

ONLINE

EXHIBITOR REGISTRATION

ONLINE

CONFERENCE DELEGATE

REGISTRATION

DOWNLOAD

BROCHURE

DOWNLOAD

FLOORPLAN

DOWNLOAD

INDIAN EXHIBITOR

FORM

DOWNLOAD

FOREGIN EXHIBITOR

FORM

DOWNLOAD

INDIAN DELEGATE FORM

DOWNLOAD

EXHIBITOR LIST

DOWNLOAD

CONFERENCE PROGRAM

SCHEDULE

CONTACT US

EMAIL:

exhibition@icerpshow.com

,

frp@frpinstitute.org

,

Info

Past Events

Organised By

SUPPORTED BY

CO – SUPPORTED BY

International Partners

Supporting Organisations

Other Supporters

Knowledge Partner

줌바 댄스 다운로드

줌바 댄스 다운로드

줌잇 다운로드

Crack for CBL Data Recovery Software 3.1.2C